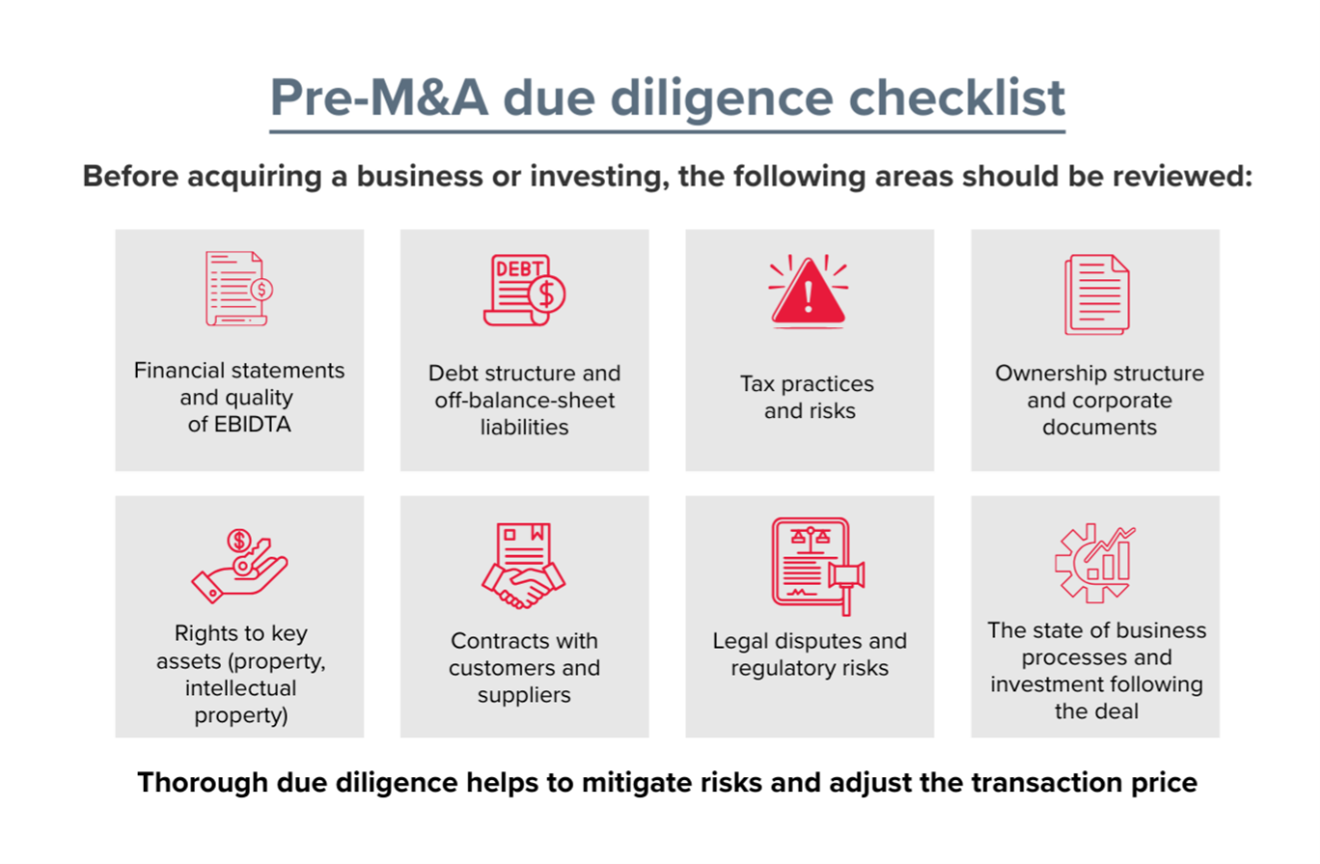

A practical due diligence checklist to review before closing a merger and acquisition (M&A) transaction, helping companies reduce risks, adjust the purchase price, and structure the deal more effectively.

The M&A market in Ukraine is gradually regaining momentum. Investment funds and strategic investors are increasingly looking for attractive assets in the context of Ukraine’s potential European integration, while companies are seeking partners and opportunities for consolidation or, conversely, the divestment of non-core assets. However, uncertainty about the future, tax and operational risks, and potential shortcomings in management or official reporting make mistakes at the deal preparation stage particularly costly. That is why a high-quality M&A audit (due diligence) is not merely a formality, but a key tool for risk management and informed deal pricing.

In a broad sense, due diligence is the process of collecting and analysing information about a business entity prior to entering into a transaction or acquiring assets. In the context of M&A, it is a comprehensive review of the target company or investment object, focusing on factors that may affect the feasibility of closing the deal, the purchase price and payment mechanism, the transaction structure, as well as the scope of warranties and the liability of the parties. Fortunately, most potential issues can be identified at an early stage of the review (except in cases of deliberate fraud). Therefore, high-quality due diligence provides a high level of assurance that the actual condition of the target will largely correspond to the terms underlying the transaction.

- Start with the right question: why do you need due diligence?

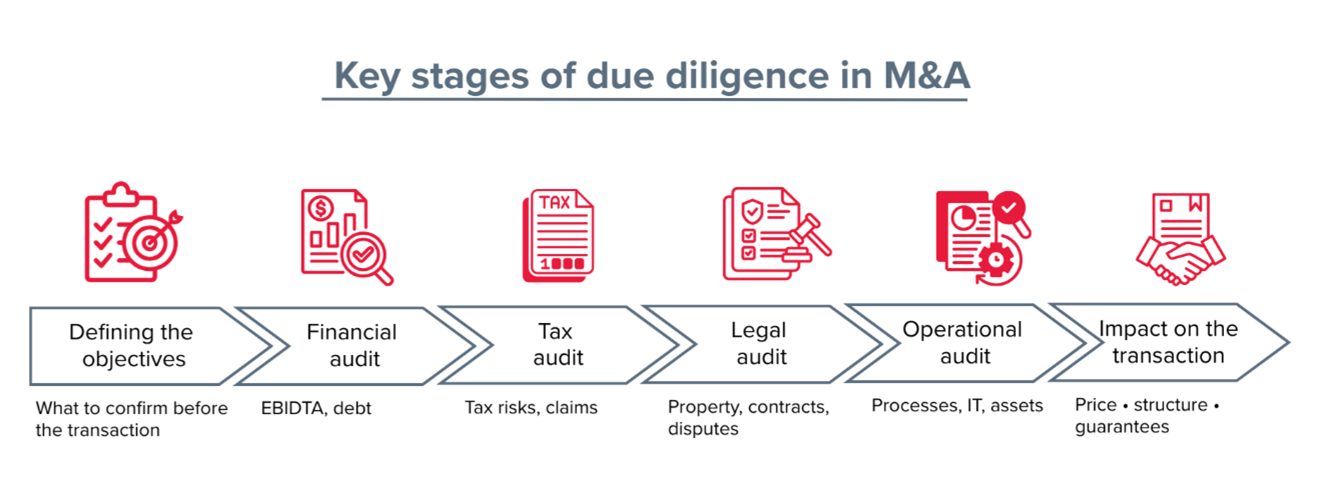

Before starting the review, it is important to clearly define what you expect to achieve from the due diligence process. For the buyer, typical objectives include confirming and clarifying the initial information about the business, identifying key risks (market, legal, tax, technological, and reputational), verifying assets and liabilities (including off-balance-sheet items, which may be difficult to detect), and assessing the potential for integrating the target into the buyer’s group.

Although the seller is the party being reviewed, it also pursues its own objectives. The main task is to present the target company as accurately and transparently as possible, minimise the scope and number of warranties, and secure the most favourable payment schedule.

Practical advice: agree in advance on the format of the final deliverable. Often, the most effective first step is a red-flag report — a concise document that outlines potential deal breakers (issues so significant for one of the parties that they may lead to termination of the negotiations) as well as other material risks. Such a report helps quickly determine whether it is worth continuing the transaction and which issues should be addressed when preparing the SPA (Sale and Purchase Agreement).

Another important step is to determine the materiality threshold (the level below which transactions are not analysed in detail), define key deadlines, and identify the main assumptions that need to be tested (for example, “the company has no undisclosed debt” or “key contracts will remain in force after the change of control”).

- Financial audit: the quality of earnings matters more than EBITDA

Financial due diligence should answer a key question: can the historical financial results be relied upon, and is there a reasonable basis to expect their sustainability in the future? The main objective of such a review is to determine whether the historical financial performance of the business is reliable. In practice, the seller may undertake certain “pre-sale” preparations: adjust commercial terms with customers, accelerate revenue recognition, defer or reallocate expenses, and enter into favourable transactions with related parties (which may not always be clearly identified as related-party transactions).

What to pay attention to:

- Data and accounting quality. If official financial reporting and actual management accounts exist in parallel, the risks increase significantly. In such cases, it becomes necessary to reconcile the two sets of data and build a consolidated view of the business from the perspective of a potential future owner, as well as assess how these differences may affect tax risks and contractual warranties.

- Adjust EBITDA / profit. Identify one-off and non-recurring transactions, the impact of intra-group transactions and changes in accounting policies, as well as any unusual cost behaviour.

- Working capital and cash flow. Review accounts receivable (delinquencies and potential uncollectibility) and accounts payable (including potential hidden liabilities), as well as inventory levels and liquidity, and the conversion of EBITDA into cash. An important element is the normalisation of working capital. Typically, the balance sheet should reflect the level of working capital required to support the EBITDA or profit level used in the company valuation. Under this approach, a working capital shortfall is usually compensated by the seller, while any surplus may either be reflected in the company’s valuation or transferred to the seller, where feasible.

- Net debt and debt-like items. In addition to bank loans, it is important to analyse guarantees, sureties, penalties, shareholder loans, lease liabilities, litigation risks, and other contingent or off-balance-sheet liabilities.

- Analysis of business drivers. Market conditions, sales dynamics and forecasts, profit margins, the structure of income and expenses, loan debt burden and financial covenants are key indicators of a company’s ability to operate sustainably after the transaction.

During financial due diligence, it is important not only to analyse primary financial information, but also to carefully assess the seller’s position. The inability or difficulty in forming a complete and transparent picture of the target’s financial performance is always a warning sign and, at a minimum, may require broader warranties from the seller.

- Tax audit: optimisation today — claims tomorrow

Tax due diligence is an analysis of a company’s tax practices and an assessment of potential claims from tax authorities, as well as the status of settlements with the state budget. Its purpose is to identify potential tax exposures and provide a monetary estimate of possible risks. These risks almost always influence price negotiations, withholding or escrow mechanisms (interim accounts used for staged payments), and the scope of the seller’s warranties. Another important aspect may be differences between the tax approaches of the seller and the buyer. In some cases, the buyer may assess tax risks more conservatively than the seller, which can lead to additional discussions during negotiations. This situation is quite common, for example, when a foreign investor acquires a Ukrainian asset.

Typical risk areas for Ukrainian companies:

- Aggressive tax optimisation or practices in the grey area (for example, the use of sole proprietors as a substitute for employment relationships in functions where such arrangements are not typical).

- Completeness and timeliness of filing tax returns and paying taxes.

- Issues with the calculation or specific practices related to the payment of corporate income tax, VAT, or excise tax (where applicable), as well as payroll taxes and social contributions on accrued salaries.

- Transfer pricing compliance and related party transactions.

- Tax audits and disputes with tax authorities, including the confirmation of tax losses and unreimbursed VAT credits (where relevant).

Practical advice: Do not limit the review to formal verification of tax returns. Try to trace the chains of tax bases and supporting documents, as well as verify the substance of transactions with significant tax impact. Be sure to evaluate current practices against your own internal policies and simulate potential claims from tax authorities for prior periods or estimate the accruals your company would record under its own rules. This analysis will form the basis for negotiations, price adjustments, and warranties.

- Legal audit: ownership rights, contracts, and ‘mines’ in corporate history

Legal due diligence assesses the legal soundness of the business, including ownership structure, asset status, key contracts, ongoing or potential litigation, encumbrances, and compliance with applicable laws and regulations.

The review typically focuses on four main areas:

- Corporate block: ownership rights to the target entity (if the transaction involves a legal entity), statutory documents, the history of corporate resolutions, powers of management bodies, existence of shareholder agreements, and off-balance-sheet liabilities (for example, golden parachutes, options, or undisclosed guarantees).

- Assets: rights to real estate and land, movable property, and intellectual property (including trademarks, domain names, and software), existing encumbrances, and risks of challenges to ownership rights.

- Contracts: clauses triggered by a change of control, restrictions or prohibitions on assignment, penalties, exclusivity provisions, long-term commitments, and currency or pricing formulas. In practice, a change of control may lead to significant deterioration in the terms of existing contracts, directly impacting financial results, which are typically the basis for valuation. The seller’s relationships with counterparties can have both positive and negative effects, but it is common practice to include requirements to negotiate with key suppliers or partners to preserve existing terms of cooperation.

- Litigation and regulatory requirements: ongoing and potential disputes, compliance with licensing and permitting requirements, and adherence to industry-specific regulatory obligations.

Practical advice: Create a list of critical agreements without which the business cannot operate or achieve its target results — such as key customer contracts, supplier agreements, leases, and financing arrangements. Review these first, as this is where the most common deal breakers are typically found.

- Operational and technical audit: assessing post-transaction investment needs

Operational (or technical) due diligence aims to determine whether the existing assets and processes align with the stated business model and to identify potential capital investments required after closing the transaction. This type of due diligence is typically conducted either by the buyer’s internal technical team or by externally engaged experts under the guidance of the technical team, as operational processes fall directly under the responsibility of the acquiring party.

What to pay attention to:

- Physical assets: condition of property, plant, and equipment; required capital investments and repair programs; and absence of critical assets.

- Business processes and controls: quality and efficiency of procurement, warehousing, sales, and production processes; dependence on key personnel or unique specialists.

- Integration with the buyer’s operations: compatibility of IT infrastructure, reporting, budgeting, corporate policies, and technical compatibility.

- Cybersecurity and IT risks: especially relevant when the business handles critical data or infrastructure; perform basic IT audits, information security assessments, or penetration testing to identify actual vulnerabilities.

Specific audits may be required for certain industries, including environmental, HSE (Health, Safety, and Environment), ESG, assessments of impact on key stakeholders, etc.

- How audit results affect the deal: price, structure, and warranties

In M&A practice, almost every target business will have some findings during due diligence. The key question is whether these findings are deal breakers or topics for discussion and negotiation.

Typical consequences of due diligence include:

- Withdrawal from the agreement or suspension until critical issues are resolved (if one or more deal breakers are identified).

- Change in transaction structure, e.g., direct acquisition of assets instead of acquiring the company that owns them, or separation of the “pure” part of the business.

- Adjustment of price and payment mechanisms: withholding part of the payment until sensitive issues are resolved (via an escrow arrangement) or contingent on achieving certain financial results (earn-out); adjusting for non-standard levels of net debt or working capital, etc.

- Review of the seller’s warranties and representations package.

A specific tool for protecting the seller is the Disclosure Letter. In this document, the seller discloses known issues or defects, and once the buyer accepts it, claims can generally be made only in relation to matters that were not disclosed.

- What sellers should prepare before due diligence: vendor due diligence and the data room

If you are a seller, proper preparation for due diligence can save months of time and significantly increase the likelihood of successfully closing the deal.

A brief checklist of key preparatory steps:

- Where possible, conduct vendor due diligence: an independent review that allows potential risks to be identified early and addressed proactively. It is crucial that such a review is performed by a third party without internal conflicts of interest inherent in management.

- Set up a Virtual Data Room (VDR): prepare a structured set of documents (e.g., registration, assets, key contracts, finance, tax, personnel, etc.). This not only allows a potential buyer to start the review quickly but also enables you to engage with multiple buyers simultaneously.

- Appoint an internal team and assign individuals responsible for data flows and liaison with a prospective buyer, providing the team with clear guidelines and incentives to achieve results.

- Agree on the basic principles and key terms of the deal before commencing full due diligence (to avoid spending resources on checks “for the sake of checking”).

- Ensure transparent communication: undisclosed facts almost always emerge later and can prove more costly at the SPA stage or in the form of honoured warranties.

Conclusion

Pre-transaction M&A due diligence focuses on mitigating risks and ensuring predictable outcomes. A well-designed due diligence process addresses three practical questions: “Is it worth acquiring?”, “What is the actual cost?”, and “How should the deal be structured to effectively manage risks?” A properly planned due diligence process saves both the buyer’s and seller’s time and resources, enabling them to reach well-founded agreements with minimal uncertainty and only the necessary level of guarantees.

If you are planning a merger or acquisition and want to assess risks before signing the agreement, professionals of BDO can assist with conducting comprehensive due diligence. The BDO team has extensive experience in financial, tax, and legal audits within the context of M&A transactions and helps investors and company owners structure deals taking into account identified risks.

Contact BDO in Ukraine for professional support during the preparation and review stages of your transaction.