In Ukraine, approaches to source documents in the context of civil law relations are being updated. The adoption of Law No. 4791-ІХ (draft law No. 14023) and amendments to Law of Ukraine No. 996 introduce new rules for day-to-day document management, particularly regarding the confirmation of work performed and services provided under civil law contracts.

What key changes to document management does Law No. 4791-IX introduce?

Recent legislative updates, particularly the adoption of Law No. 4791-IX and amendments to Law of Ukraine No. 996, simplify the documentation of transactions under civil law contracts. The principle is straightforward: fewer formalities — more focus on ensuring that transactions are genuine and properly substantiated. Under the new rules, if a source document contains information on the date or period of service provision, performance of work, or tenancy, the absence of a signature or other details from the customer (or tenant) will not be considered a violation of source document requirements. However, this simplification can only be applied if two conditions are met:

- The procedure for recording business transactions is established in a written agreement between the parties.

- The business transaction is recorded in the accounts in the period in which it occurs.

Is it possible to operate without work completion or services provided certificates under the new legislation?

Law No. 4791-IX allows for the possibility of not issuing c work completion or services provided certificates under civil law contracts — provided this is explicitly stipulated in the contract and the parties have agreed on an alternative method to confirm the fulfilment of obligations. In other words, “waiving certificates” is not automatic: the contract must clearly specify which document (or set of documents) confirms the provision of services or completion of work, the transaction completion date, and the acceptance procedure (for example, the time limit for objections and default acceptance).

The amendments to Law of Ukraine No. 996 further allow the provision of services to be documented by an invoice issued and signed by the service provider. Provided that the invoice contains all mandatory details of a source document (identification of the parties, date/period, description and scope of services, cost, currency, signature or identifier of the responsible person) and there is a clear link to payment, such an invoice may be recognised as a source document for accounting and tax purposes.

In international practice, an invoice is a document issued by the seller to the buyer, listing goods and services, their quantities, and the price at which they are supplied. It also includes details of the goods, delivery terms, and information about the sender and recipient. Issuing an invoice indicates that the goods have been dispatched according to the agreed delivery terms and that the buyer is obliged to pay, except in cases of prepayment. For services, issuing an invoice confirms that the services have been provided. In other words, an invoice serves as confirmation of the dispatch of goods or the provision of services.

Legal grounds for waiving the requirement for completion certificates: viable possibilities and limitations

Waiving the requirement for completion certificates is only possible by mutual agreement between the parties. This must be explicitly stated in the contract, and such an agreement must not conflict with the law. In gig contracts or agreements with sole proprietors, the parties may specify that an invoice, email correspondence, or other document/action (e.g., confirmation on a platform) serves as proof of work performed or services provided. It is important that the contract clearly defines the conditions and mechanism for acceptance — this is what gives such confirmation the necessary legal force.

In doing so, this option does not apply to transactions for which the law establishes specific documentation requirements, such as:

How do you draw up a civil law contract without certificates?

To apply the simplified documentation rules, this must be agreed upon with the other party in the contract. The contract must be in writing — either on paper or electronically; the key point is that it must be written, not verbal. To ensure that business transactions are properly documented without certificates, it is recommended that:

- Specify in the contract in advance the procedure for confirming the completion of work or the provision of services (e.g., invoice, email, platform signature, report). Clearly state that the parties recognise the legal validity of source documents related to services, work, leases, and tenancies (invoices, certificates) even if they do not include the title, surname, handwritten or digital signature of the authorised representative of the service recipient, contracting party, lessor, or tenant.

- Ensure the retention of supporting materials, such as correspondence, screenshots, or confirmations from platforms/services.

- Use electronic document management to automate and control processes.

This approach helps prevent disputes, provides a solid evidential basis for tax authorities, and improves accounting efficiency.

Tax risks associated with using invoices as source document

Using invoices as source documents helps simplify accounting, but it also introduces certain tax risks:

- Tax authorities may request additional evidence of the actual performance of work or services (e.g., reports, photographs, correspondence, or signed documents).

- The absence of supporting documents in certain situations may make it more difficult to defend your position during an audit or dispute.

- It is important that the invoice includes all mandatory details and is supported by other evidence.

EU practice: confirming the performance of work in Poland, the Czech Republic, and Lithuania

Experience in several EU countries, such as Poland, the Czech Republic, and Lithuania, shows that an invoice is often sufficient as a source financial document to confirm the provision of services or performance of work in the B2B sector. However, it is generally not used in isolation and is accompanied by other evidence of the actual fulfilment of obligations.

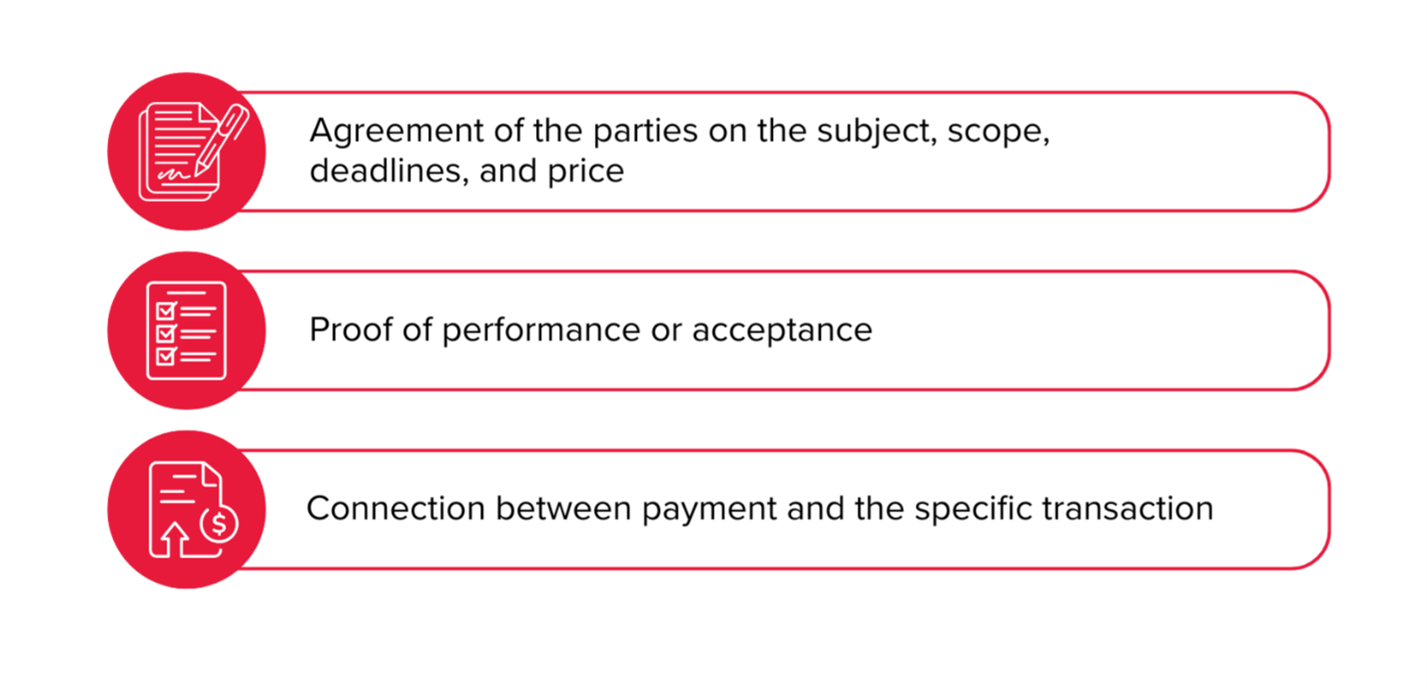

In practice, regulatory authorities and courts focus on the existence of a “body of evidence” confirming:

Such evidence typically includes a contract or offer and a detailed order (e.g., SOW, PO), correspondence regarding agreement on scope and deliverables (emails or messaging apps), deliverables in the form of reports, timesheets, file transfers, or access grants, confirmation of acceptance of the deliverables (particularly via electronic document management platforms and electronic signatures), and payment documents enabling the transaction to be clearly identified. For Ukrainian companies, this approach is particularly useful: specifying in the contract exactly which document(s) and in what manner confirm the completion of work, establishing materiality thresholds, and retaining supporting evidence of performance. Adapting these practices to Ukrainian regulations allows companies to benefit from deregulation opportunities without compromising the quality of the evidential base during tax audits or disputes.

The materiality criterion as a tool for managing document flow

Considering the changes introduced by Law No. 4791-IX and the updated Law of Ukraine No. 996, it is advisable to implement the materiality criterion within a company’s internal policies as a key tool for managing document flow and tax risks. This approach aligns with general accounting principles, particularly the principles of rationality and substance over form.

For business transactions involving insignificant amounts (approximately UAH 5,000 to UAH 10,000, depending on the scale of operations), using an invoice as the source document may be both economically justified and sufficient, provided it includes all mandatory details and the transaction is confirmed by payment.

Moreover, for transactions involving substantial amounts, or for transactions with a higher level of tax or legal risk (e.g., new counterparties, transactions with non-residents, intangible services, or creative and consultancy work), it is advisable to retain a work completion certificate as additional evidence of the validity of the business transaction. In such cases, the certificate serves primarily an evidential purpose rather than a formal one, strengthening the taxpayer’s position during tax audits or legal disputes.

Introducing the materiality criterion allows for a differentiated approach to transaction documentation, enabling accounting and legal departments to focus their resources on genuinely high-risk transactions. As a result, an entity achieves a balance between the simplification of document flow promoted by the legislator and maintaining an appropriate level of tax prudence, which is essential for the financial security of the business.

How to avoid disputes regarding the completion of work

It is important to consider the risk of unilateral interpretation of work completion. If one party considers the work to have been completed while the other does not agree, the absence of acceptance certificates may complicate the resolution of the dispute — primarily due to the lack of an agreed acceptance date and clear criteria for assessing the outcome.

To minimise such risks, it is advisable to define a clear mechanism for confirming completion in the contract in advance: what constitutes the result, in what form and to whom it is delivered, who is responsible for acceptance, and what requirements apply to comments.

In practice, this may take the form of a “default acceptance” procedure: the contractor sends an invoice or report and a notification of completion, and the client has, for example, 5–10 working days to submit substantiated objections, listing any defects and specifying a deadline for their rectification; if no objections are received within this period, the service is deemed accepted. Additionally, the contract may provide for automatic acceptance upon payment (or upon partial payment for a specific stage), a mechanism for phased or partial acceptance, as well as a rule stipulating that communication regarding acceptance must take place only through specified channels with mandatory confirmation of receipt.

Such detail reduces the scope for manipulation, makes the acceptance procedure more predictable, and simplifies the process of proving that the work has been performed in the event of a tax audit or legal dispute.

The position of government authorities on the adopted law

- Ministry of Economy: updates on support for Bill No. 14023 and the abolition of the requirement for certificates of completion

- State Tax Service Main Office in Vinnytsia Region (06.03.2026): clarification on the application of Law No. 4791-ІХ, particularly regarding the possibility of a primary document being signed by a single responsible person on behalf of the contractor, subject to contractual agreement.

Conclusions and Practical Recommendations

- Focus on substance rather than formalities in documentation.

It is important to have evidence that the service or work was in place: what exactly was done, when, to what extent, and what was paid for. It is not so much about “which document” as “what it confirms”.

How this works in practice: alongside the invoice, keep the agreed terms of reference or scope of work in your correspondence, confirmation of delivery of the result (file, access to a repository, link to the task), as well as a timesheet or a brief report on what was done during the period.

- It is possible to work without acceptance certificates, but only if this is explicitly stipulated in the contract.

Waiving acceptance certificates is not an automatic process: the parties must agree in advance and clearly specify in a written contract how performance is to be confirmed. In this model, the invoice may serve as the source document; however, it is advisable to support it with additional documentation (SOW/PO, correspondence, reports/timesheets, confirmation of delivery of results or access, payment documents).

How to formulate this: for example, “confirmation consists of invoice + payment” or “invoice + email/acceptance notice”, and in the absence of objections within X days, the service is deemed accepted. It is also advisable to specify the list of supporting documents: SOW/PO, timesheet, links to Jira/Asana, bank statement with a clear payment reference.

- The materiality criterion is helpful: for smaller amounts, a simpler set of documents is sufficient; for significant or high-risk amounts, a more comprehensive set is required.

A practical approach: set an internal threshold (for example, UAH 5,000–10,000) and use it to determine the level of documentary evidence required. If the amount or risks are higher, it is advisable to prepare a certificate or another acceptance document. Separately, it is worth considering exceptions where special rules apply (public funds, state/municipal leases, construction contracts, donations, charitable and humanitarian aid).

Example: a one-off service for UAH 5,000–10,000 — an invoice, payment, and a brief report or correspondence are often sufficient. For a project worth UAH 300,000 or involving a new counterparty or non-resident, it is better to have an invoice + certificate (or acceptance report) + results of the work. For construction contracts and public funds, special forms or acceptance procedures are usually required.

Summary: Law No. 4791-IX, together with the amendments to Law No. 996, provides businesses with greater flexibility: an invoice can serve as proof of service provision, and a certificate of completion is not always required. However, this does not eliminate risks automatically. The most reliable protection is a well-drafted contract, clear internal procedures, and properly documented evidence of actual performance.

A practical checklist for companies to ensure controlled and predictable document flow

In short — steps to maintain a controlled and predictable document flow:

- Update contract templates: specify how performance is confirmed, how results are accepted, where confirmations are sent, and the timeframe for raising objections.

- Define a “materiality” threshold and a simple risk matrix: consider factors such as amount, type of service, new counterparties, non-residents, and intangible deliverables.

- Compile supporting documents for invoices: include SOW/PO, correspondence, reports/timesheets, confirmation of delivery/results access, and payment records.

- For large or high-risk transactions: retain an acceptance certificate or protocol as additional evidence.

- Check for exceptions: if dealing with budget funds, state/municipal leases, construction contracts, donations, etc., stricter rules may apply.

The law provides greater freedom—and with it, greater responsibility. By setting rules for document acceptance, defining materiality thresholds, and retaining supporting documents in advance, you make document management simpler and more predictable, both in daily operations and during audits.

When will the documentation simplification changes take effect?

The President signed the law on 16 March 2026, and on 17 March 2026, Law of Ukraine No. 4791-ІХ dated 24 February 2026 was published, amending Article 9 of Law of Ukraine No. 996-XIV “On Accounting and Financial Reporting In Ukraine” dated 16.07.1999. The changes will come into force on 1 April 2026.

The experts at BDO in Ukraine assist companies in assessing the risks of using invoices as source documents, adapting civil law contracts to comply with the new legal requirements, and developing an effective internal document management system that balances streamlined procedures with appropriate tax compliance.

If your company is planning to revise its approach to documenting business transactions or wants to verify whether its current document management system meets the new requirements, contact the experts at BDO in Ukraine for professional guidance.